- 7 Minute Read

- 11th February 2024

London's Flexible Office Market in 2024: A Detailed Report on Prices, Trends, and Usage Insights

The UK's office culture is transforming, with the traditional concept of 'office space' evolving into a more fluid and adaptable model. Once characterised by the fixed leases of Central London and major regional cities, the office sector is now embracing flexibility. This metamorphosis, accelerated by the pandemic, has seen the office market adapt to the demands of a modern workforce.

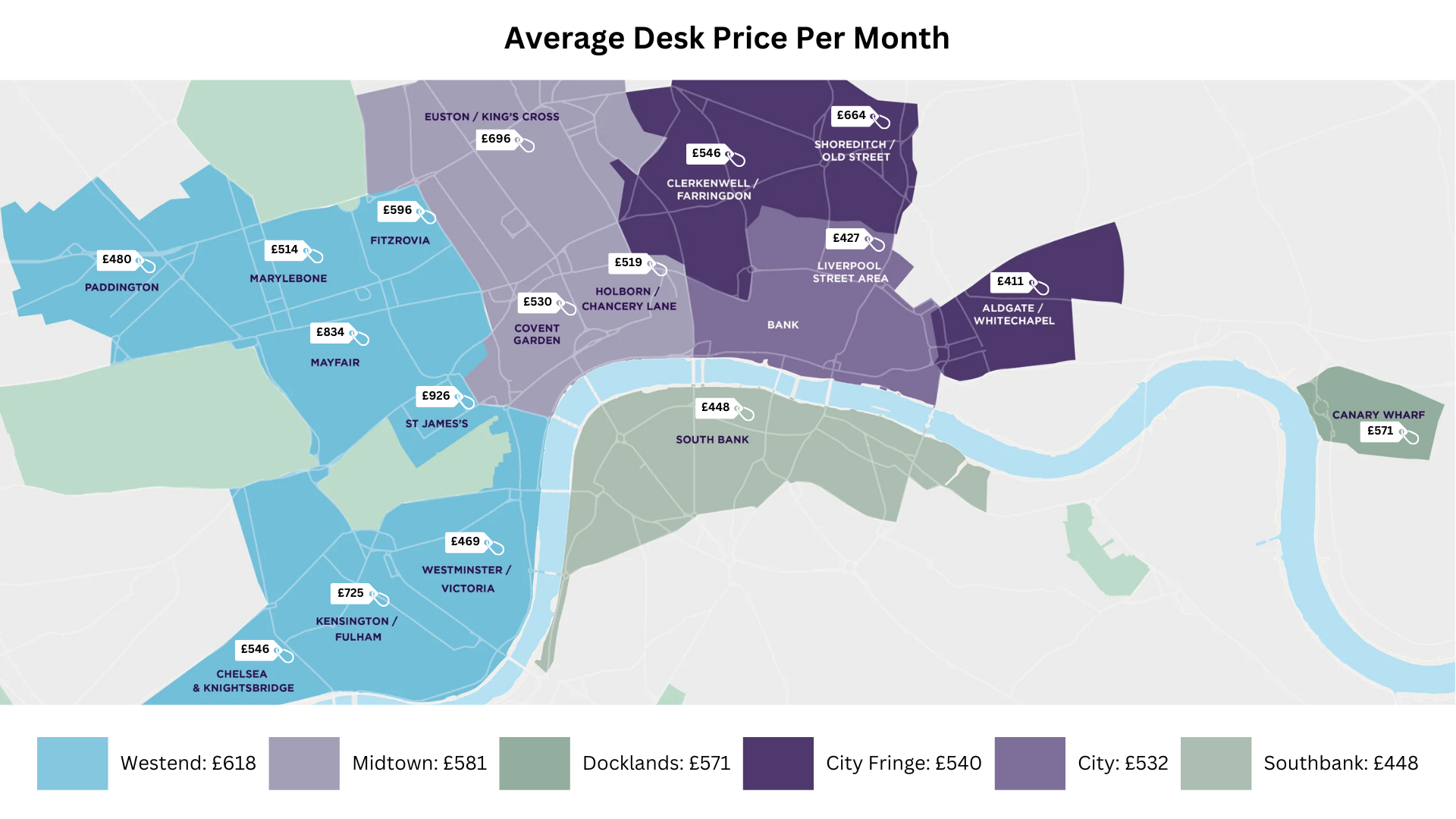

Central London's sub-markets, such as the West End and Midtown, have been at the forefront in terms of desk pricing and tenant mix in recent years. The traditional industry boundaries have blurred, evidenced by some hedge funds migrating from Mayfair and St James’s to Covent Garden and some tech firms establishing themselves in Fitzrovia rather than the Clerkenwell / Old Street / Shoreditch “tech-belt”.

Desk cost dynamics

Premium areas

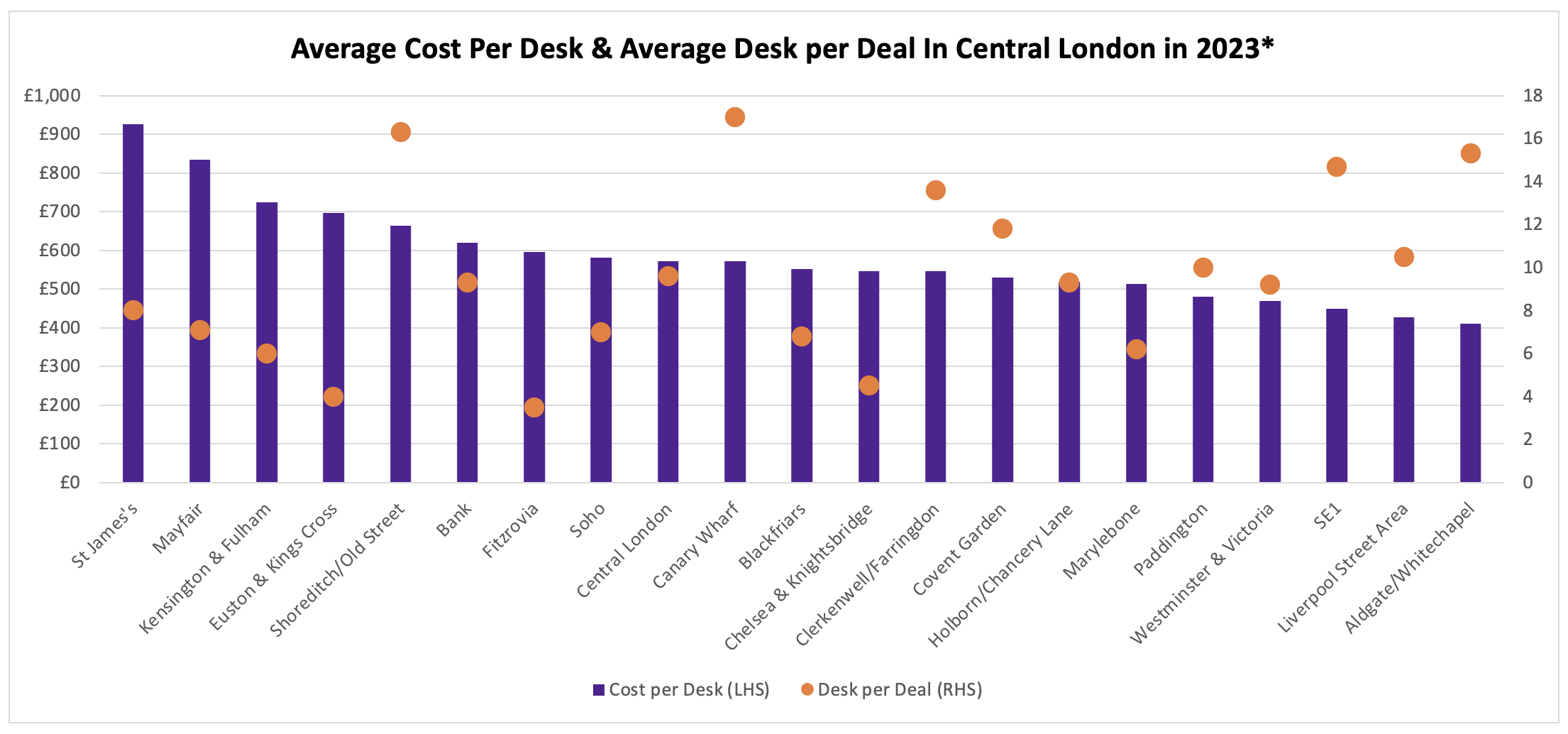

In 2023, the West End districts of St James's, Mayfair, and Kensington, stood out, with the average cost per desk amounting to £926, £834, and £725, respectively.

Growth trajectory

Rental trends have been influenced by factors such as supply dynamics and property quality. Limited availability in the West End and Kings Cross contrasts with oversupply in the City and South Bank sub-markets. Moreover, the emergence of high-spec, energy-efficient buildings around the City Fringe is enhancing the quality of offerings and pushing rental values upwards, thanks to strong demand for the best space in the market.

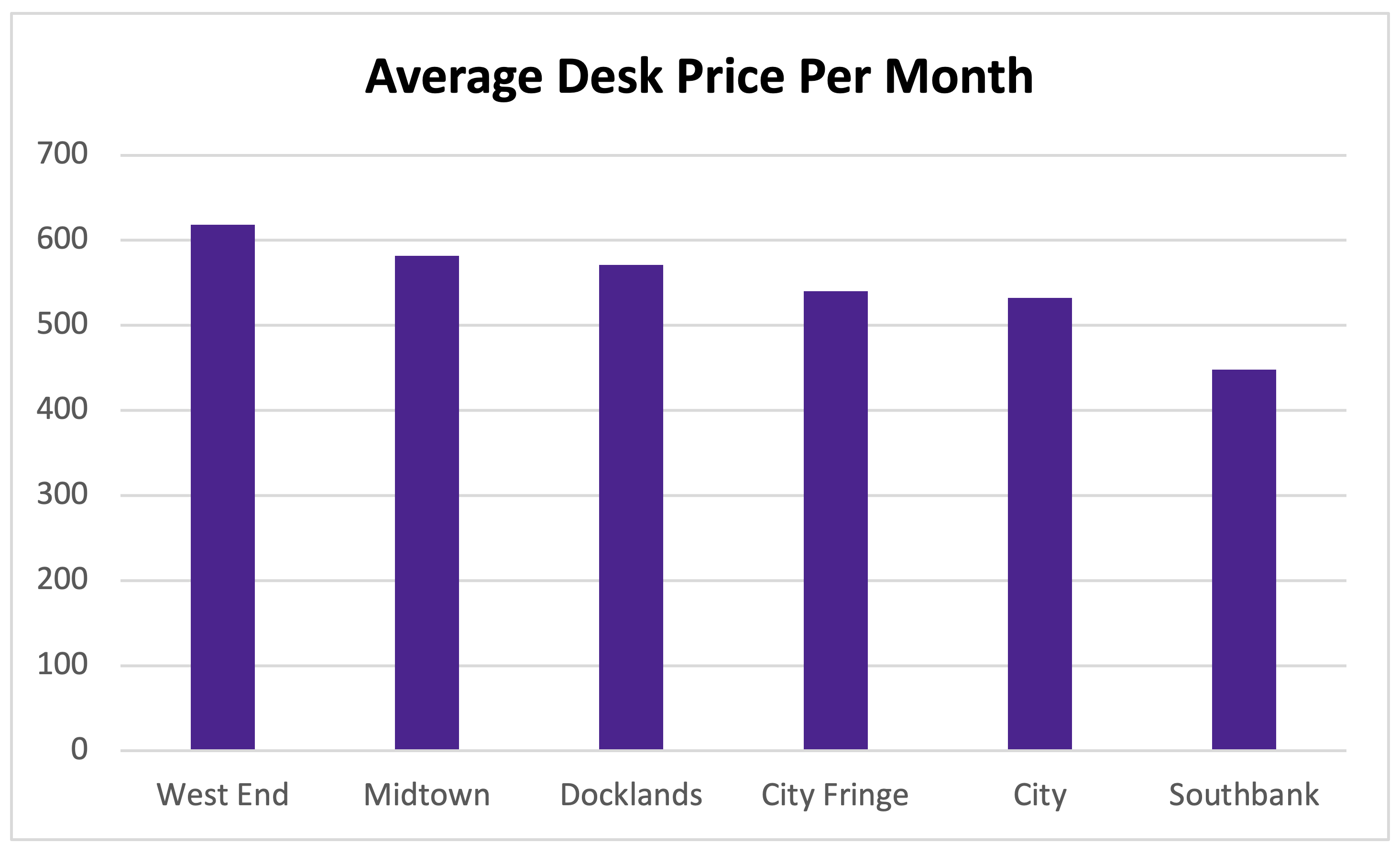

Some Central London submarkets, such as the West End and Midtown, recorded positive growth in recent years, while others, such as Southbank and the City, have seen average cost per desk going in a downward trajectory of late.

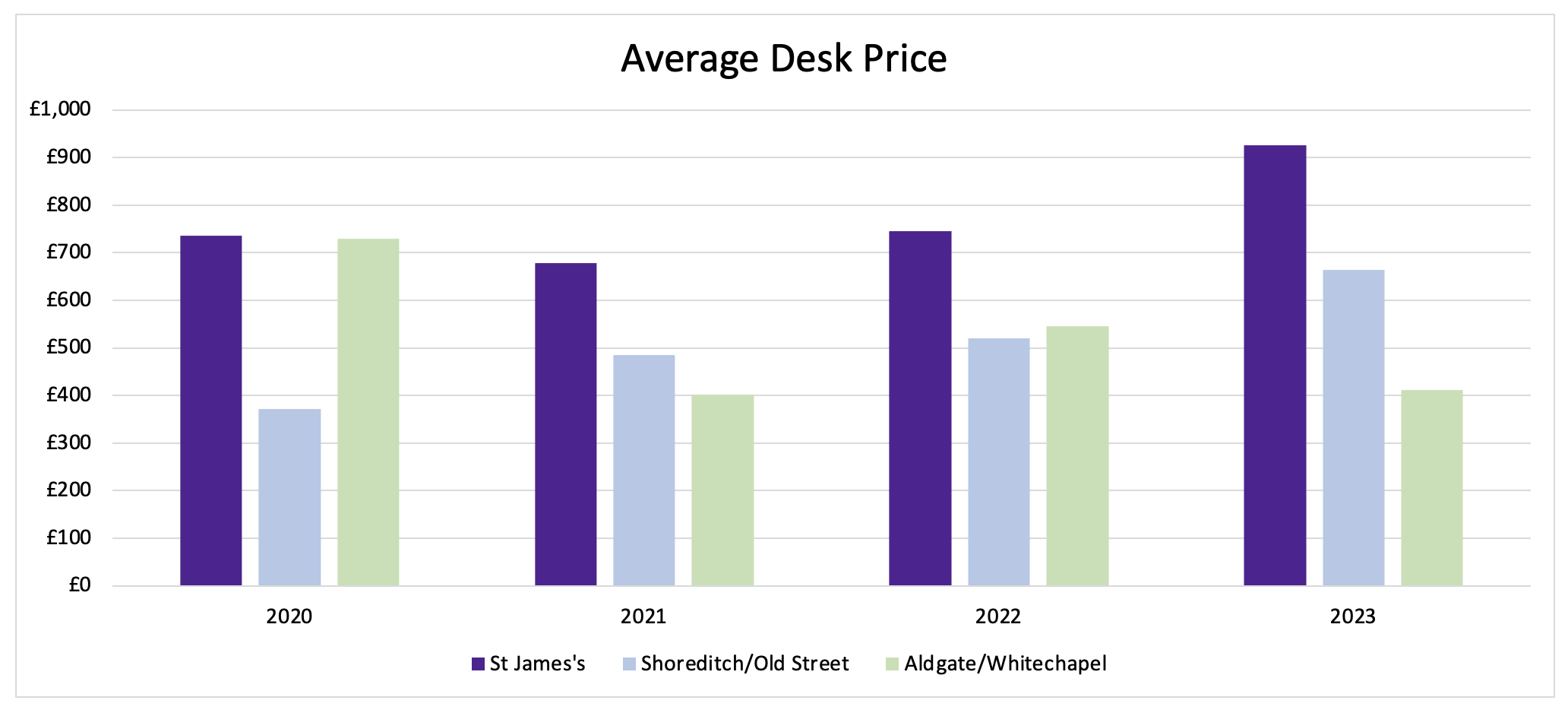

Certain districts, notably St James's and Shoreditch/Old Street, have seen a surge in desk prices from 2020 to 2023, reflecting the growing demand in both districts and the premium nature of the former.

Range of costs

However, average costs per desk per month vary between locations. SE1, Liverpool Street and Aldgate were among the most affordable Central London areas in 2023, recording average rents of £448, £427 and £411, respectively. Outside the West End, areas such as Euston, Kings Cross, Shoreditch and Bank have witnessed among the highest costs per desk this year, achieving an average of £696, £664 and £620, respectively.

"Demand for London office accommodation is being driven, in part, by the operators of serviced and co-working office space that are seeking accommodation for conversion, reflecting the robustness of occupier demand in that market sector."

- Ollie Lee, Carter Jonas

St James's saw a 26% increase from £735 in 2020 to £926 in 2023, while Mayfair experienced a rise of 16.6% from £715 in 2020 to £834 in 2023.

The areas of Aldgate/Whitechapel and Liverpool Street have grappled with an oversupply, partly due to the influx of larger managed spaces as several new buildings have opened their doors recently. Intense competition among landlords has escalated incentives, prompting considerable rent concessions for tenants.

The remarkable 79% surge in Shoreditch is largely owing to market dynamics have been significantly influenced by WeWork's strategic rent increases since 2020. While WeWork's recent filing for administration has cast a shadow over the sector, the flexible office industry remains well-positioned for growth, with businesses seeking adaptable workspaces that can cater to their evolving needs.

Leasing trends

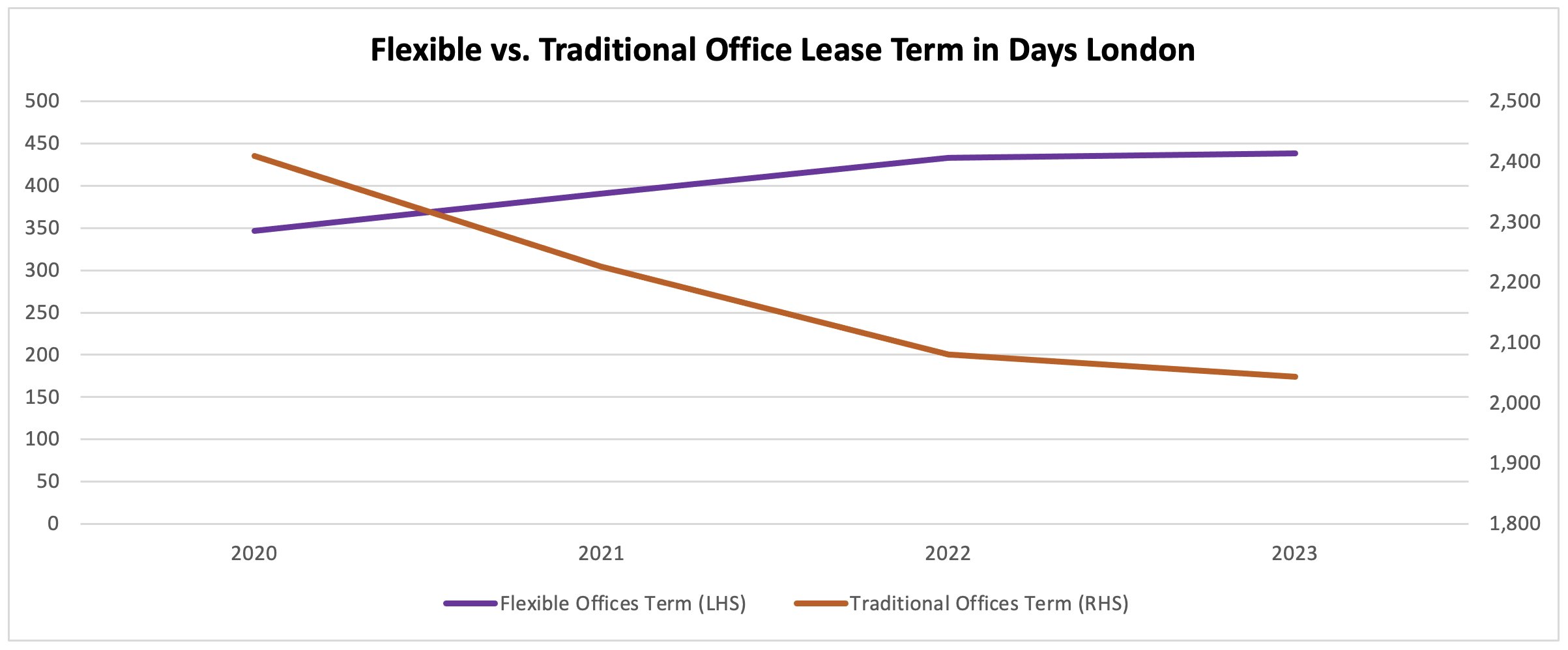

Lease Terms and Time from Initial Enquiry to Move-in

Duration dynamics

The lease term for flexible space has been on an upward curve in Central London, moving from 347 days in 2020 to a recent peak of 438 days in 2023. In contrast, the traditional office lease term in Central London has decreased in the same period, with an average term of 2,409 days in 2020 falling to 2,044 in 2023. However, the lease length for both types appears to be levelling off in recent months.

Transition efficiency

Concurrently, the time from lead to move-in in the capital has decreased from 100 days in 2020 to 61 days in 2023, suggesting faster decision-making and possibly a streamlined administrative process. Smaller requirements and fewer options in the market have also contributed to the decrease in the time from lead to move-in.

"An increasing number of landlords of non-serviced office suites, typically below 5,000 sq ft, are fitting out available accommodation and offering it to let on a “plug-in-and-go” basis to compete with the serviced office market."

- Ollie Lee, Carter Jonas

Desk per deal analysis

Growth pockets

Canary Wharf and Shoreditch/Old Street have experienced a notable increase in the average number of desks per deal from 2020 to 2023. This trend points towards a growing preference among larger companies for these areas, likely driven by the greater availability of spacious premises.

"While there has been a steady growth in new serviced office buildings, a large part of the growth in flex space has been due to managed office spaces. Many landlords are now offering fitted, all-inclusive, self-contained spaces, on shorter-term deals. This part of the flex market will continue to grow at pace throughout 2024."

- Jon Posener, COO of Office Freedom

The average number of desks per deal in Central London vary across areas,

Canary Wharf showed a significant increase from 4.6 desks in 2020 to 17 desks in 2023. Companies including WeWork, The Office Group and SQB have all opened new flexible centres in Canary Wharf in that period, providing much-needed high-quality space in the area.

Shoreditch/Old Street maintained steady growth, with 12 desks in 2020 and 16.3 desks in 2023, supported by larger tech companies looking for space in the area.

Blackfriars, Fitzrovia, Holborn/Chancery Lane and Soho recorded a notable decrease in average desk per deal in 2023 compared to 2020. A lack of available high-quality larger floorspace in Soho and Fitzrovia, is likely to be one of the reasons behind the fall in those areas. In contrast, Holborn/Chancery Land has seen a number of large buildings opening in 2023.

Diverse Occupier Landscape in Central London

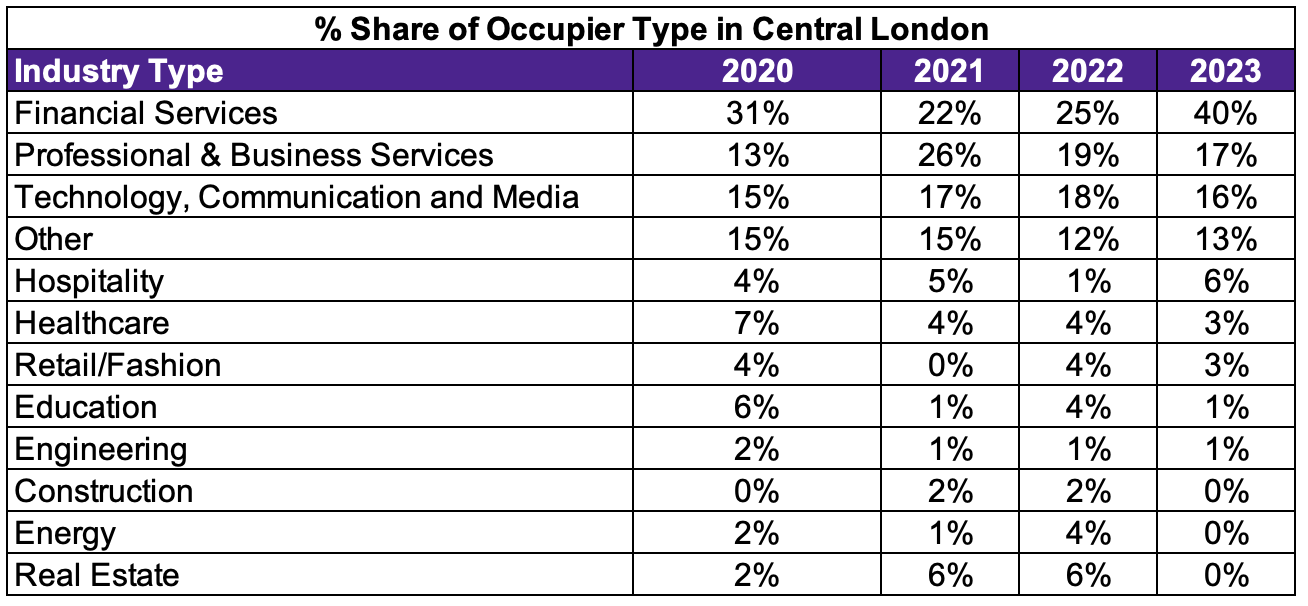

In Central London, the Financial Services industry also occupied the largest share of traditional office space leased in 2023, accounting for 40% of the total. Other sectors taking a significant share of the traditional offices' take-up were Professional & Business Services (17%) and Technology, Communication and Media (16%).

Notably, most Real Estate occupiers who took traditional leases in 2023 were flexible space providers and accounted for 7% of the total office take-up in that period, showing the current demand for flexible space in the market.

The data paints a vivid picture of the occupier landscape in Central London

Financial Services

Dominating the scene, their presence has grown from 31.48% share of the total in 2020 to a commanding 40.00% in 2023, although it shrank significantly in 2021.

TMT

Despite a decrease from 18% in 2022 to 15.7% share in 2023, the technology, communication and media sector remains among the largest occupiers in London.

Professional & Business Services

This sector has remained among the most active having 17% of the share in 2023.

Supply

Growth of new flex centres since 2021

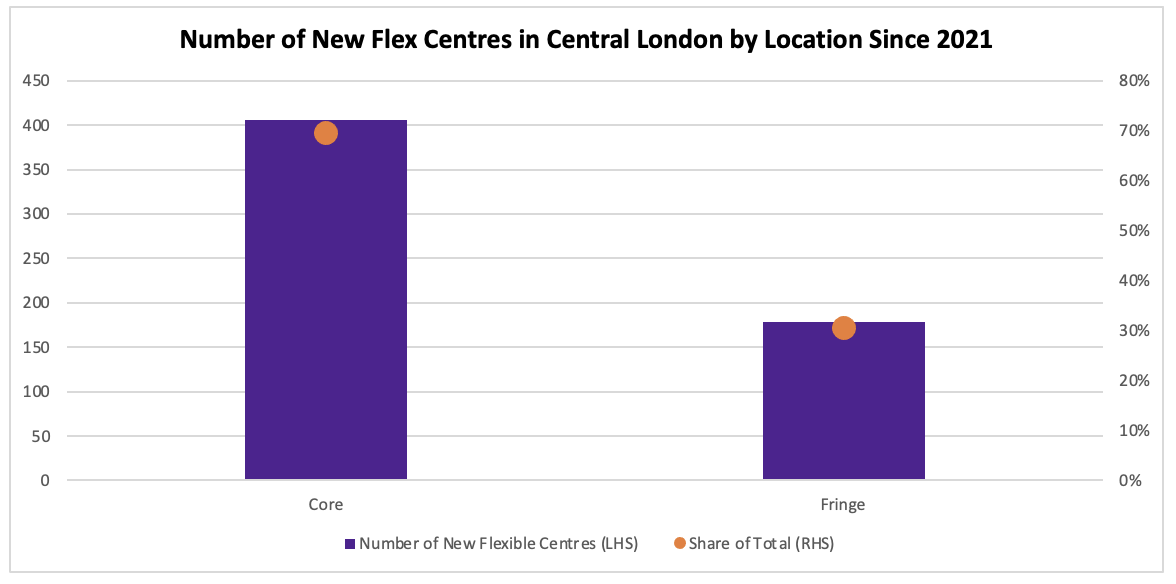

Central London led the growth in flex space, with 586 new flex centres opening in the period 2021 – September 2023, accounting for 80% of the new openings across the UK. Core markets in the capital accounted for 70% of the new spaces, while the fringe locations accounted for the remainder.

Central London new centres by area year on year

The City of London saw the most significant growth, with six new centres in 2021, 26 in 2022, and 82 in 2023. Shoreditch/Old Street and SE1 also witnessed a substantial increase in the same period.

"It feels that the flex market has now recovered from Covid. Regardless of what happens with WeWork, there is now a large amount of established flex office operators who continue to grow. There is still some hesitancy from certain companies in terms of coming back to the office, but we are finding that the majority of our clients have been embracing a more hybrid working policy and are taking permanent office space."

- Richard Smith, CEO of Office Freedom

Conclusions

Central London has witnessed growth in flexible workspace pricing, with areas like St James's, Mayfair, and Shoreditch leading the charge. The significant price surges in these districts from 2020 to 2023 highlight the increasing demand for premium, flexible workspaces.

However, it's essential to note the challenges. While some areas have seen a surge in demand and pricing, others, like Aldgate/Whitechapel and Liverpool Street, have experienced a decline. These fluctuations emphasise the importance of understanding local market dynamics and the factors influencing demand.

The occupier landscape in Central London has remained similar to three years ago, with Financial Services taking a dominant position. The continued demand from those occupiers suggests that businesses across sectors recognise the benefits of flexible workspaces.

Beyond the capital, other significant cities in the UK are also seeing a marked interest in flexible workspaces. The data indicates that while Central London remains a dominant player given its overall size relative to the regional markets, cities/towns such as Reading, Aberdeen, and Cambridge are carving out their own significant niches in the flexible workspace sector. This suggests a broadening of demand, with regional hubs increasingly becoming focal points for businesses seeking adaptable office solutions.

In the broader context, the pandemic has undeniably acted as a catalyst, accelerating the transition towards flexible workspaces. As businesses prioritise adaptability, cost-efficiency, and employee well-being, the demand for flexible workspaces is poised to grow further.

Continue reading our report on UK’s flexible office workspace here

This report delves into flexible workspaces across the UK, examining key drivers such as cost per desk, deals per desk, lease lengths and supply in Central London and other significant urban hubs. The report has been written in collaboration with Carter Jonas, one of UK’s leading property consultancies, enabling deeper insight and analysis into the sector.